I’ve been reading Freaks of Fortune, a wonderful book on the history of the modern insurance industry. It’s a fascinating survey of the emerging capitalist threads of the 19th Century and their implications for the world in which we live. There are too many points to summarize or opine on for one short blog post, but a few concepts jumped out at me (quoted as screenshots below). I’ll split them up into a few posts, so that I can tell the stories well.

First, modern insurance came from underwriting a very specific peril, universally understood to be the most dangerous thing about commerce: the sea. Disease at-sea, storms, navigation errors, sharks, and pirates were the biggest threat to commerce originating in London, where the insurance industry had its origins.

The concept of a ‘risque’ (sic) was a financial asset representing the insurance interest in the face of perils at-sea. Our modern concept of risk, particularly in a financial sense, only made thin and vague sense to many 19th century merchants. The economy before the first industrial revolution was made up almost entirely of individual local craftsmen, artisans, and farmers. There were uncertainties associated with crop yields, but not much else when it came to commerce, and certainly not such that it had to be organized. Dutch East India Company, the first corporation, and the organization to establish one of the earliest ever stock exchanges**, became a corporation in the first place as a way to diversify risk of individual ships encountering peril at sea.

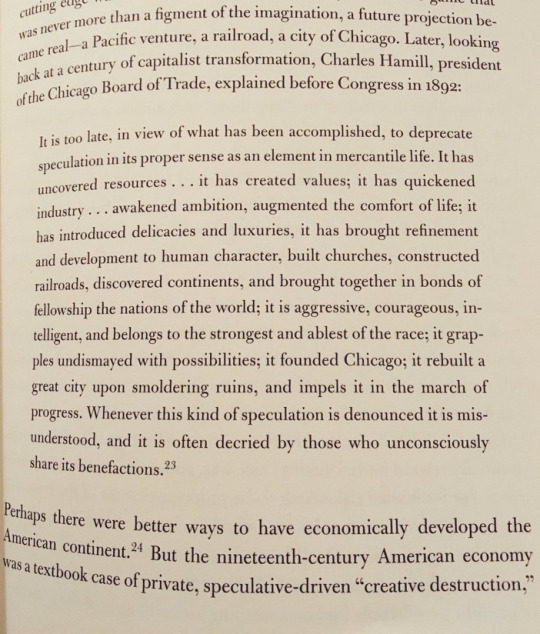

As seafaring trade grew, risques became a more popular asset, but the concept behind them needed to be argued for, even by the industrialists who wanted to extend rail lines or expand oil territory. The president of the Board of Chicago Trade had to present to Congress on the value of risk-taking and speculation in markets as late as 1892:

As the concept of risk itself took on a more philosophical, cultural point of view, its application thusly broadened. We take risk for granted today, but it’s fairly new, and still not evenly understood or appreciated—it’s a big part of what makes Silicon Valley so successful. Often, in describing how I think about investing in and working on startups, it feels as though I am describing alien concepts, particularly when I speak about a power distribution curve. Indeed, if I could point to any one cultural condition that is endemic to the Silicon Valley that I haven’t seen anywhere else, it is this: the incredible amount of fault tolerance. We have optimized conditions for creating hypotheses, and learning whether those hypotheses have merit. Edison’s quotation feels appropriate, to this point: “I have not failed. I’ve just found 10,000 ways that won’t work.”

Even still, I continue to believe that in Silicon Valley we don’t take nearly enough risk. We pattern match, and optimize for downside, and subconsciously try to validate our myopic positions, and engage in highly social and mimetic behavior. I’m guilty of all of those things as much as anyone. But I happen to believe that the old saying that there are only a dozen great startups per year (is that the latest number? it keeps rising) would be dramatically higher, if we were willing to take more risk. I think the bulk of the responsibility on this note falls to LPs and GPs. If we funded more “unproven” managers or more “contrarian” founders, I’m convinced that we would find more amazing companies. Risk is a powerful force, and we have only started truly learning about it in the last 3-4 generations. We have learning yet to do.

**Florentine and Venetian merchants also purported to have a version of a stock exchange in the early 1400s, as well, if you’re curious about this stuff, too. But check out Freaks of Fortune, first.