They call it a Cambrian moment. These days, every city worth its salt comes with a startup ecosystem: co-working spaces and accelerators mark emerging hubs across the United States and around the world. Since The Social Network, high school students have grown up with the legend of the college dorm room startup as a central narrative. From healthcare to insurance to apparel to food, it seems as though there is a startup for every piece of our economy today, and 10 more behind each one. They seem to be everywhere.

In recent years, the number of new venture capital firms has exploded, raising to hundreds of new fund formations a year. My Limited Partner friends tell me they see 300+ new fund pitches per year. Accelerators are rising follow-on funds, athletes are raising side project funds, and scout programs are launching as standalone platforms to fund the early stage. Meanwhile, the late stage has similarly continued on a great fundraising run: there have been multiple multi-billion dollar funds closed, Softbank has committed $200B into the ecosystem, and the middle eastern sovereign capital pools are investing heavily into tech. And there seems to be no end to growth in the space: as global yield stays low, hundreds of billions of assets are looking for a home, and finding promise in the global tech sector. Startups. What’s more, after the global financial crisis in 2008, large corporations had shrunk, Millennials were graduating into uncertain job markets. Youth unemployment was startlingly high, from Spain to Iran to South Africa, and everything in-between. Necessity is the mother of invention. Of course, startups rushed in to fill the void.

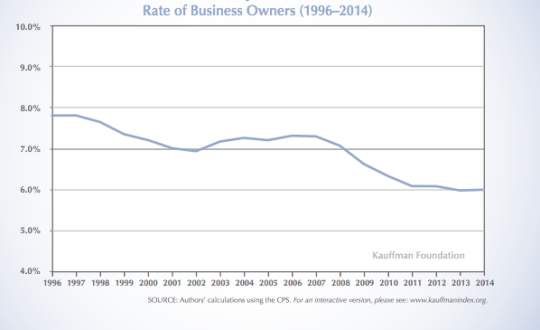

Or have they? Take a look at this chart, published by the Kauffman Foundation in this great research report (pdf link) about new business creation in the United States:

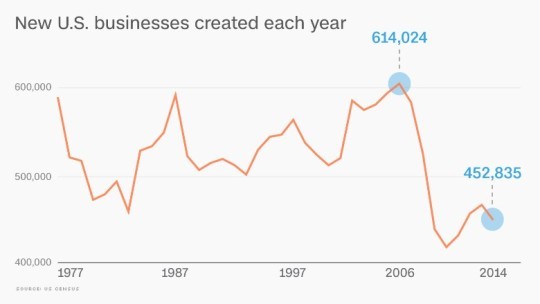

It shows that the rate of business owners nationally has actually fallen by over 20% since 1996, with an even more precipitous decline in 2008. So first of all, more startups weren’t created after 2008. Dramatically fewer were. And while new business formation has rebounded since 2008, it is still lower than it was 30 years ago. But take a look at the chart below, from the U.S. Census Bureau, and you’ll see that, in fact, new business formation in the United States is at a 40-year low!

So what gives? I conclude a few things:

First of all, the word startup has taken on a special connotation, and implies the formation of a unique type of company. I’m not convinced by this formulation: 7-Eleven was venture-backed. Blue Bottle Coffee was a venture-backed company. The fastest growing company over the last five years, by revenue, was a Utah-based bootstrapped multi-level marketing company called Younique Products. It was founded in 2012, and had $400 million of revenue by the end of 2016. Seriously. Look it up. So– any business can grow fast and deliver 20x, 30x, etc. Any notion that there is a certain *type* of company that is venture fundable is flatly wrong. But this mindset is particularly relevant among venture capitalists lately. My friend Satya captured it well:

while there is more money than ever in VC there is also more risk aversion and less independent conviction. stranding many companies that are building solid businesses in “out of favor” markets or in markets where “venture scale returns” are not a straight line path.

— Satya Patel (@satyap)

Word. In fairness to venture capitalists, liquidity has been particularly hard to find lately, which may be affecting how they think about deploying their capital. The hive mind is more intense in venture capital today than it has been in my 7 years in the business. Valuations have been blown out of proportion among “fundable” companies, while those with promising but early trajectories, those with ambitious but workmanlike metrics, are perennially struggling to raise capital. My favorite quotation to capture this phenomenon is: deals these days are badly undersubscribed until it is badly oversubscribed.

Second of all, the United States is in a period of possibly the most intense consolidation in the innovation and technology ecosystems since the 1870′s –– when, in an effort to entice European businesspeople and workers to the United States, *massive* government contracts were granted to corporations to fund expansion of the United States project, leading to the passage of the Sherman Antitrust Act in 1890. Look at the top companies in the United States by market capitalization: if you take out oil companies and investment corporations, you have Apple, Google, Microsoft, Facebook, Amazon. Semil Shah covered how their presence affects startup investing (https://stratechery.com/2016/how-fangam-impacts-startups-how-startups-adjust-to-fangam-investing-in-a-fangam-world/), but it’s worth noting that the phenomena that have lead to these companies’ massive, immense success is not isolated to them. The network effect, and the focus on consumer surplus as a means of crowding out competition, is endemic to the software-enabled innovation company today.

Competition and capitalism are actually not compatible, as Peter Thiel might say. And network effects, focused on consumer surplus, scalable demand generation, and very thin aggregation of crowds, are a *really* good manifestation of capitalism. Why start your own private practice, when economies of scale make lifestyle better to be part of a network? How do you open a small business when a big network-based company is offering a cheaper service? How do you find an edge in technology spaces that require data, when the incumbents have all the network effects and incredible expertise in attacking adjacencies?

Finally, given both of the former two points, there is a broad-based misunderstanding about startup formation today. People say: “Cloud-based services make it easier than ever”. “Pre-seed capital invests earlier”. “More funds than ever before”. But the truth is, the *vast* majority of capital that invests in startups comes after the critical period that matters most for startup founders: the “friends & family round”… the “just bootstrap it” round… As we all know, most Americans can’t afford an unexpected expense of $400. And as I’m sure most of us can intuit, the ability to raise a “friends and family round” is not evenly distributed according to talent. So taking a year, 6 months, or even a quarter, to quit your job and start a new business is simply a nonstarter for most Americans today. In a world where the small business bank loan has all but evaporated (particularly post-2008), many Americans – and others around the world – aren’t starting companies because they just can’t afford to. When we talk about diversity in tech, I’m interested in hearing about the structural impediments to startup success. Ultimately, many of them can be boiled down to access to capital. Large, urban coastal centers are attracting capital and resources aplenty, while mid-sized and middle-of-the-country towns are not keeping apace. Within those urban coastal centers, wealthy, well-connected, mostly white males are raising more and more capital at higher and higher valuations, while other demographics are not keeping apace. Even within the demographics that overindex in startup formation, there is a very strong sense of “haves” and “have-nots” which is intensifying, even in the midst of a lot of noise about diversity and startups. This is pushing inequality further, slowing our ability to innovate writ large, and keeping too many Americans outside of equity participation in this country. Economists across the political spectrum will agree that new job growth comes from new business formation. And businesspeople of all stripes will tell you that equity upside is the most important input for building wealth. This isn’t just a matter of building cool technology – though that is impacted, as well – this is a matter of how nations can grow to be healthy, and supportive of their citizens. I was pleased to read Sam’s post American Equity yesterday, as its clear he recognizes the same issue I do. The central planning and policy-prescriptions for this issue should range from ideas like his, to the varying universal basic income (UBI) concepts, to investing in incentives for banks to lend for small business formation. All of this is good. But the market driven approaches will need to supplement these – frankly, the central planning approaches will need to supplement the market driven approaches. And this starts with recognizing where we *actually* are. I’ve spoken to too many people in the tech world who say there are “too many funds” or “not another app”.

Quite the opposite, if you ask me.