Take a look at Capital And Main for the podcast version of this, and the original appearance of these ideas, among far more interesting ones. And to it…

Whether it takes 15 years or 50, it is almost certain that self-driving cars will be on the road within my lifetime. Waymo, the Alphabet company, is at 3 million test miles driven. Uber, BMW, Cruise (in partnership with General Motors), Mercedes, Volvo, Nissan, Ford, and others have also been logging hundreds of thousands of miles with no one behind the wheel. Tesla drivers, meanwhile, have notched 300 million miles using the company’s Autopilot autonomous driving feature.

At the exponential pace of software adoption, the technology is nearly ready for the road. But technological hurdles are one thing; cultural barriers are bound to prove far trickier to overcome.

A 2017 study by Deloitte found that three-quarters of Americans do not trust driverless vehicles. The American Automobile Association found that 54 percent of drivers feel less safe even sharing the road with fully autonomous cars. But how safe is safe enough?

To better understand this question – the main question causing vexation among insurers and others – think about the psychology of the driver. Implicit in my decision to get on the road and drive is an understanding that there are other drivers on the road, as well. And every interaction with another moving vehicle is an exercise in game theory: that is, intuitively modeling what I expect the other driver to do as a function of what I’m going to do. Yet how does game theory work with a self-driving car? Am I supposed to anticipate what an algorithm would do?

Self-driving cars tend to come in fleets. Each one is automatically part of a network of others that share its software. This allows the machine learning processes to run at the rate of *all* the driving data captured by all the cars on the road, instead of just one.

This also means that the cars can talk to each other at the speed of a super-fast wireless connection. In an interaction between two self-driving cars, the game theory is not between them, but between the entire fleet and any other entity, since they have perfect information about each other. Imagine being a driver, then, and approaching an intersection where all the cars know exactly what the others will do. Of course, each self-driving fleet will have its own software, and thus far, there is no sign that there will be any integration between different company fleets. So, the likelier scenario is: You approach an intersection, and you don’t know if the cars are talking about you or not. And if they are, what are the saying? Now consider a split-second decision at high speeds, or in confined space. Unnerving, right?

Each year, more than 30,000 Americans die and many more are injured in car accidents, the vast majority of which are caused by human error. Driverless cars could eliminate 90% of these deaths and injuries, according to experts. But these numbers—impressive as they are—may not matter very much.

The fear of a road full of self-driving cars is a fear that machine game theory, even if it is explicitly designed to avoid accidents, is not perfectly compatible with human empathy. And in the moments of inconsistency, what will the robot do? For example: If there is a chance to protect two pedestrians, but it requires potentially injuring a rider, which does a fleet of self-driving cars choose? What if you’re the one sitting in the passenger seat? Colloquially, ‘what if the software malfunctions?’ gets at the same point. Human malfunction is reasonably predictable. I know that accidents happen when a driver is drunk, distracted, sleepy, or overly upset. But what might cause a machine to crash—literally? Being unable to relate on a human level makes it much scarier, even though the reality may be much safer. Solving the social resistance to self-driving cars (beyond concerns that they could cost millions of jobs) will not come down to safety statistics, or even to miles driven without incident. Those don’t actually matter nearly as much as policymakers and technologists think. Signaling, and communicating a clear sense of fairness – and if not empathy, then something that rhymes with it – will matter much more.

Thanks to Rick Wartzman at Capital and Main for editing and publishing me on this one!

They call it a Cambrian moment. These days, every city worth its salt comes with a startup ecosystem: co-working spaces and accelerators mark emerging hubs across the United States and around the world. Since The Social Network, high school students have grown up with the legend of the college dorm room startup as a central narrative. From healthcare to insurance to apparel to food, it seems as though there is a startup for every piece of our economy today, and 10 more behind each one. They seem to be everywhere.

In recent years, the number of new venture capital firms has exploded, raising to hundreds of new fund formations a year. My Limited Partner friends tell me they see 300+ new fund pitches per year. Accelerators are rising follow-on funds, athletes are raising side project funds, and scout programs are launching as standalone platforms to fund the early stage. Meanwhile, the late stage has similarly continued on a great fundraising run: there have been multiplemulti-billion dollar funds closed, Softbank has committed $200B into the ecosystem, and the middle eastern sovereign capital pools are investing heavily into tech. And there seems to be no end to growth in the space: as global yield stays low, hundreds of billions of assets are looking for a home, and finding promise in the global tech sector. Startups. What’s more, after the global financial crisis in 2008, large corporations had shrunk, Millennials were graduating into uncertain job markets. Youth unemployment was startlingly high, from Spain to Iran to South Africa, and everything in-between. Necessity is the mother of invention. Of course, startups rushed in to fill the void.

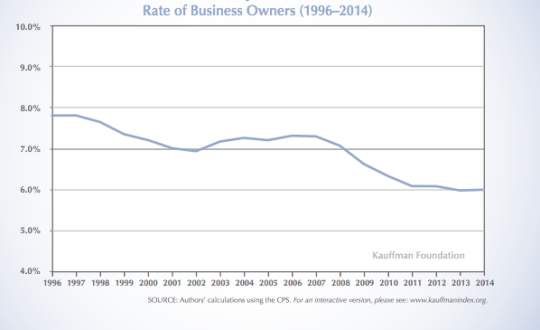

Or have they? Take a look at this chart, published by the Kauffman Foundation in this great research report (pdf link) about new business creation in the United States:

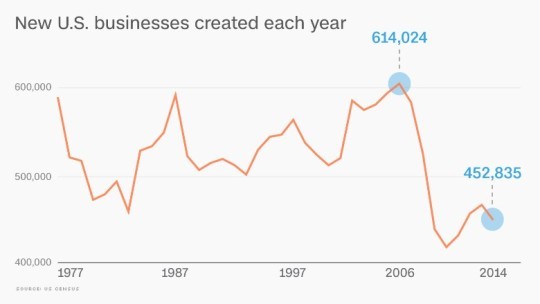

It shows that the rate of business owners nationally has actually fallen by over 20% since 1996, with an even more precipitous decline in 2008. So first of all, more startups weren’t created after 2008. Dramatically fewer were. And while new business formation has rebounded since 2008, it is still lower than it was 30 years ago. But take a look at the chart below, from the U.S. Census Bureau, and you’ll see that, in fact, new business formation in the United States is at a 40-year low!

So what gives? I conclude a few things:

First of all, the word startup has taken on a special connotation, and implies the formation of a unique type of company. I’m not convinced by this formulation: 7-Eleven was venture-backed. Blue Bottle Coffee was a venture-backed company. The fastest growing company over the last five years, by revenue, was a Utah-based bootstrapped multi-level marketing company called Younique Products. It was founded in 2012, and had $400 million of revenue by the end of 2016. Seriously. Look it up. So– any business can grow fast and deliver 20x, 30x, etc. Any notion that there is a certain *type* of company that is venture fundable is flatly wrong. But this mindset is particularly relevant among venture capitalists lately. My friend Satya captured it well:

while there is more money than ever in VC there is also more risk aversion and less independent conviction. stranding many companies that are building solid businesses in “out of favor” markets or in markets where “venture scale returns” are not a straight line path.

Word. In fairness to venture capitalists, liquidity has been particularly hard to find lately, which may be affecting how they think about deploying their capital. The hive mind is more intense in venture capital today than it has been in my 7 years in the business. Valuations have been blown out of proportion among “fundable” companies, while those with promising but early trajectories, those with ambitious but workmanlike metrics, are perennially struggling to raise capital. My favorite quotation to capture this phenomenon is: deals these days are badly undersubscribed until it is badly oversubscribed.

Second of all, the United States is in a period of possibly the most intense consolidation in the innovation and technology ecosystems since the 1870′s –– when, in an effort to entice European businesspeople and workers to the United States, *massive* government contracts were granted to corporations to fund expansion of the United States project, leading to the passage of the Sherman Antitrust Act in 1890. Look at the top companies in the United States by market capitalization: if you take out oil companies and investment corporations, you have Apple, Google, Microsoft, Facebook, Amazon. Semil Shah covered how their presence affects startup investing (https://stratechery.com/2016/how-fangam-impacts-startups-how-startups-adjust-to-fangam-investing-in-a-fangam-world/), but it’s worth noting that the phenomena that have lead to these companies’ massive, immense success is not isolated to them. The network effect, and the focus on consumer surplus as a means of crowding out competition, is endemic to the software-enabled innovation company today.

Competition and capitalism are actually not compatible, as Peter Thiel might say. And network effects, focused on consumer surplus, scalable demand generation, and very thin aggregation of crowds, are a *really* good manifestation of capitalism. Why start your own private practice, when economies of scale make lifestyle better to be part of a network? How do you open a small business when a big network-based company is offering a cheaper service? How do you find an edge in technology spaces that require data, when the incumbents have all the network effects and incredible expertise in attacking adjacencies?

Finally, given both of the former two points, there is a broad-based misunderstanding about startup formation today. People say: “Cloud-based services make it easier than ever”. “Pre-seed capital invests earlier”. “More funds than ever before”. But the truth is, the *vast* majority of capital that invests in startups comes after the critical period that matters most for startup founders: the “friends & family round”… the “just bootstrap it” round… As we all know, most Americans can’t afford an unexpected expense of $400. And as I’m sure most of us can intuit, the ability to raise a “friends and family round” is not evenly distributed according to talent. So taking a year, 6 months, or even a quarter, to quit your job and start a new business is simply a nonstarter for most Americans today. In a world where the small business bank loan has all but evaporated (particularly post-2008), many Americans – and others around the world – aren’t starting companies because they just can’t afford to. When we talk about diversity in tech, I’m interested in hearing about the structural impediments to startup success. Ultimately, many of them can be boiled down to access to capital. Large, urban coastal centers are attracting capital and resources aplenty, while mid-sized and middle-of-the-country towns are not keeping apace. Within those urban coastal centers, wealthy, well-connected, mostly white males are raising more and more capital at higher and higher valuations, while other demographics are not keeping apace. Even within the demographics that overindex in startup formation, there is a very strong sense of “haves” and “have-nots” which is intensifying, even in the midst of a lot of noise about diversity and startups. This is pushing inequality further, slowing our ability to innovate writ large, and keeping too many Americans outside of equity participation in this country. Economists across the political spectrum will agree that new job growth comes from new business formation. And businesspeople of all stripes will tell you that equity upside is the most important input for building wealth. This isn’t just a matter of building cool technology – though that is impacted, as well – this is a matter of how nations can grow to be healthy, and supportive of their citizens. I was pleased to read Sam’s post American Equity yesterday, as its clear he recognizes the same issue I do. The central planning and policy-prescriptions for this issue should range from ideas like his, to the varying universal basic income (UBI) concepts, to investing in incentives for banks to lend for small business formation. All of this is good. But the market driven approaches will need to supplement these – frankly, the central planning approaches will need to supplement the market driven approaches. And this starts with recognizing where we *actually* are. I’ve spoken to too many people in the tech world who say there are “too many funds” or “not another app”.

They are the among the only lasting advantages in business – particularly in the fast-moving technology environment. And the question about how to grow one is one of the most common pain points for someone early in their career, particularly if they did not get lucky and choose the right company to work for, where the network was built-in for them.

So here’s a word: most people wrongly focus on the “network” side of the equation before the “proprietary” side. It’s relatively easy to guess somebody’s email address. And it’s a toss up who will respond to a cold email. It’s relatively easy to meet a luminary – attend the right conference, hang around after she speaks, you may get 5 minutes. But if you do this before the “proprietary” part, you’re getting it backwards.

Proprietary, in this context, means you are known *for something*. You are useful, have an expertise, or even simply a well-researched interest somewhere. If you reach out to me as someone generally interested in getting ahead, why do you stand out over any other person who shares that desire? But if you are yourself an expert, or have a truly differentiated point of view, then it’s a different game – you’ll often find they actually want to meet you as much as you want to meet them.

If you want to build out your network, step one: stop networking. Practice thinking independently; reading, writing, and building. Become the most interesting person in your field.

In an influential 1979 behavioral economics paper, Daniel Kahneman and his colleague Amos Tversky developed “Prospect Theory” as a way to make sense of decision-making. The summary of the paper was, if I may, that humans do not make optimal decisions, which normative (”should”) frameworks suggest, but instead have irrational aversion to certain losses, and minimize the probability of other losses.

Here’s an example:

Here, Kahneman (via Thinking, Fast and Slow) outlines the cases where a decision-maker irrationally minimizes potential losses versus maximizing potential gains. As the theory goes, humans sometimes choose to be risk-averse, even it results in an unfavorable outcome. The opposite also applies: we sometimes are risk-seeking even if it results in an unfavorable outcome. The intersection of actuarial science and behavioral economics purports to find itself in the bottom right box. You choose to buy insurance, which is $1 more than the statistically-adjusted cost of “going for it” because of the fear of losing $10,000. At least, that’s how the model suggests it would be, right?

It is illegal to drive without auto insurance in all 50 states of the country today. The penalties range per state, but it is on the order of $150 to $1000 for a first offense, and in some states even a month’s imprisonment! And yet, in 2012, 1 in 8 motorists were uninsured.* That number is high enough to suggest that the bottom right quadrant of the matrix above does not apply as cleanly as we would hope it to. Some drivers, of course, flatly can’t afford a monthly payment, or have a risk calculus that combines the risks relating to auto insurance with other financial risks in their lives. That is to say, it’s impossible to know what everybody’s short term financial needs are; walk a mile in another man’s shoes, right? But nonetheless, many drivers are simply risk seeking in a way that breaks even this probability distortion model. Of course, the whole point of prospect theory is that actual decision-making includes a variety of probability distortions and mental shortcuts. And in this case, even when it is mandated by law, with a financial penalty not only for accidents, but also for non-adherence, double digit-percentages of drivers still go without auto insurance. Mental shortcut, indeed. Health insurance, which is (for now) mandated by federal law, has comparable adoption numbers. The uninsured rate for health insurance was 11.9% in 2012.**

The insurance policies that people buy often fall into two categories. One: mandated by law, with scary non-adherence implications; two: mandated as a means to accessing something else you really want, like a house or an apartment. Other than that, many consumers choose to wing it, either because there are short term cash needs which appear more pressing, or because they believe it “wouldn’t happen to them”. These behavioral quirks in our psychology are really important for insurance tech companies to study, and learn well. Insurance tech is very “hot” right now. Many startups are thinking about the great ways that usage-based insurance, flexible and tied to smaller, more granular actions, can be more efficient, empowering, and consumer-friendly. They’re right. But we think we’re safer, healthier, and better protected than we are. So, a caution in designing your business model to account for what will likely be expensive customer acquisition. A caution in designing technocratic policies, especially if you’re going to model consumer behavior. Insurance is sold, not bought.

Two anecdotes stuck out to me in Derek Thompson’s Atlantic post about “The Four-Letter Code to Selling Just About Anything.”

First, the concept that people prefer the image of themselves in the mirror to that in photos. I certainly do, and often feel like I look lopsided in photos. But that makes sense, since I’m seeing the mirror image of what I’m used to seeing. I imagine the same applies to the phenomenon of hearing one’s voice (which happens far less often). If you are used to hearing it come from your own mouth, with the baritone coming from your lungs, the nasally effect manifesting in your own nose, et cetera, that is the familiar sound and so something close, but not quite there, is jarring.

Second, the clustering of popular names: Derek describes research done by Stanley Lieberson which concludes that “Most parents prefer first names for their children that are common but not too common, optimally differentiated from other children’s names. This helps explain how names fall in and out of fashion, even though, unlike almost every other cultural product, they are not driven by price or advertising. “

Our subconscious does more work than we give it credit for, and drives the ‘facts’ which we accept in product design, brand development, fashion, food, and even what constitutes ‘beauty’. As per this article, we all share a programmed yearning for familiarity, but perhaps not at the conscious level. That familiarity, developed in our early evolution, establishes trust. But too familiar, and our conscious brain kicks in, as we also want individuality, and the ability to be unique in our expression and decisions. MAYA, or “most advanced yet acceptable” is Raymond Loewy, the iconic 20th century industrial designer’s, framework for describing this exact concept.

I always used to find it funny that so-called “creative types” dressed in similar ways, or how uniform the “alternative kids” trope was across American grade schools, or how certain typefaces fall into favor (or out of it, Comic Sans) in the name of “good design”. Why is the Scandanavian aesthetic, and mid-century modern furniture, found in so many Millennial households today?

Two easy conclusions come to mind.

First, beauty and style are often not so subjective as we let ourselves believe, but in fact follow a form that maps to the nature of our social psychology and neurology. We value belonging and the feeling of independence, and a healthy tension between those in a brand creates conditions for a consumer to fall in love with an aesthetic.

Second, given a formal structure to beauty and style, one can actually change the conditions for beauty, so long as she hews to the frameworks that motivate people. Recommendation and matching engines are not new in Internet history: digital advertising and e-commerce businesses have used behavioral psychology to design experiences that will optimize access to the consumer wallet. Pandora (and now Spotify, Apple, and other streaming radio services) can pick something I will probably like well, at this point. But these achievements only goes so far as curation. I wonder: can a software program design an aesthetic from scratch? 2016 was a landmark year for Artificial Intelligence interfaces taking market share in the consumer landscape, from customer service to scheduling, from health coaching to search. I have yet to see an AI-designed aesthetic that has succeeded, but the above suggests that the conditions for it are within reach.

It seems inevitable to me, then, that we will soon be able to develop technology can automatically design a sound, an image, or even a space, to appeal to the subjective mind. I wonder, as that time approaches, whether there is a greater premium on actually being truly unique in brand and design, rather than simply derivative, rather than anchoring in the familiar. My colleague Morgan wrote a thoughtful meditation about how odd truly transformative inventions look at first.

Over the holiday I was catching up on the unread articles in my browser (time to switch to Pocket/Instapaper… there were almost 100) and I bumped into this one by Bloomberg collecting venture predictions for the most important trend of 2016.

I really liked Rebecca’s comment: “2016 was the year the internet quietly sped up″ and haven’t been able to get it out of my head. In the venture community, we often credit Amazon Web Services – and the rise of cloud computing more generally – as an inflection point in the startup industry, as a founder could build a technology company for the cost of a subscription to EC2, instead of having to buy and maintain their own servers and manually include CPU, memory, PCI components, et cetera. This is the difference between $100,000+ for your own hardware and $1000+ for access to a subscription. The floodgates burst open with startup activity, and the world was never the same. Crazy as it sounds now, perhaps it will have been Jeff Bezos’ most valuable contribution to the technology community during this period.

When the 200 millionth 3G handheld device shipped in 2007, days before Steve Jobs went on stage to announce the iPhone, another inflection point occurred: the birth of mobile as we know it today. Most people ascribe all the value to the iPhone 1, incorrectly. Yes, touch screens and the concept of the app were transformative, but it was actually the iPhone 2 that I find most interesting, and that actually represents the true inflection point: the iPhone 3G. In that moment, connection speeds were fast enough that ‘real-time’ was within reach for applications, GPS and turn-by-turn navigation arrived (at scale) on a handheld device. And it was only in this context that UberCab made sense. And only in the release, the next year, of the iPhone 3GS, where the camera finally was usable, where Instagram made sense.

LTE, whose adoption reached interesting scale some time in late 2009/early 2010, took the evolving speed characteristics to the next step, whereby a piece of media wouldn’t have to buffer for long periods to load, where the expectation was instantaneous and continuous media. It’s only in this environment – a matter of telecommunications standards having been adopted widely enough, where true shopping and banking on the phone were not unreasonable, where constant multimedia communication made unit economic sense – where Spotify and Snapchat were possible.

As 4G adoption takes hold, and live video streaming and realtime video chat explode on Facebook, Snapchat, and the new players Marco Polo, House Party, Tribe continue their blistering growth, we have our resilient and fast-improving infrastructure to thank for the rewiring of our user experiences with these devices.

5G (the G simply stands for generation, FYI) is around the corner, and upload and download speeds are north of 50 Mbps for many connections today, such that the “always-on” connection that we have come to expect from Wifi will be possible with standard mobile devices as well. In this sense, it may be that the Internet of Things was indeed a bit early, but not simply because the killer use cases hadn’t arrived, as many have speculated, but actually because the infrastructure wasn’t ready yet. I also believe the internet of Things is a massively correct trend, but we’re not thinking small enough or big enough – stay tuned for a post on the latter, but as a teaser, consider the notion of data centers that are themselves mobile (read: self-driving cars/trains, UAVs). I’m imagining a dynamically updating, fully mobile cloud that moves data packets between the physically closest points, across a mesh, or *incredibly* cheaply, as the servers themselves move humans and cargo. Imagine what kind of application layer that technology will enable. Distributed computing on crack!

I’m endlessly excited about companies that are accelerating users up the Internet access curve, and about companies that are steepening the internet access curve itself. While we quarrel over social psychology and culture as the driving forces of adoption, the infrastructure layer may be the most important precondition for timing an information technology movement.

The rise of populism, right-wing candidates, and unpredictable jingoism has been correlated in the past with financial crises (quite closely, in fact). My friend Cathy did a great job of exposing this correlation, and noting that perhaps we shouldn’t be surprised about what’s happening in Austria, in Britain, in Italy, France, Germany, and of course the United States. But the surprise, for me, lies elsewhere. A broad swath of U.S. economists would have claimed, as recently as weeks ago, that the 4.3% national unemployment rate, hundreds of thousands of new non-farm payroll based jobs created every month, and slow but steady GDP growth were representative of an economy in steady hands, in good and improving shape. While the global financial crisis “wiped off 13% of global production and 20% off global trade" including scores of defaulted mortgages, student loans, and stable jobs. But they came back, didn’t they? The stock market hit all-time record highs in 2016, didn’t it? So are we recovering or not? Is it a weak recovery or a strong one? Is this actually a financial crisis?

The rise of income inequality is one suggestion that something is very, very off: while unemployment is low, there are is still 7.4 million Americans who are jobless, and in the meantime, the corporate profits, heights in the stock market, and low interest rates mean that those with means have been able to invest and take leverage on their dollars to accelerate their wealth, while leaving others out. My colleague Morgan published a brilliant report describing the changing nature of the equity markets: as companies go public later, only private investors get access to some of the most dynamic upside and growth of these companies. Thus, those who have assets to qualify as accredited investors (millionaires, basically) can participate, and the rest of the population, who might simply want to invest or grow their savings cannot. A few days ago, I tweeted a passing thought about the challenges with buying a house a few days ago and was stunned by the response to it:

I was naive about how many people’s first house down payment was made by their parents until fairly recently. Wealth really is longitudinal.

The examples are endless. Income inequality is the phrase we use as a placeholder to describe what should better be described as “wealth and income inequality”. Assets, clinical health, and access to the knowledge economy– or at least access to opportunity– are insufficiently measured in “income” but are matters of wealth. But if we are so close to full-employment, the level of wealth inequality that would qualify as crisis would have to be profound. Is that where we are? Possibly. And this is bad. Poverty is not simply a matter of basic human needs, but of context. There is a joke in Manhattan that two doctors who send their child to private school feel poor. But there’s something to it. Inequality is socially corrosive, and leads to conflict and drags down the health of entire societies. Richard Wilkinson, an epidemiologist, does great work researching and describing this phenomenon.

Another suggestion is wage stagnation. Jobs have come back, with hundreds of thousands added to the economy almost every month for the last 5-6 years. Wages, however, have remained flat. Whichever jobs left during the Great Recession of 2008 were not replaced with jobs that paid as much, or whose wages grew apace. While some critics point out that 2002 to 2015 saw wage growth higher than inflation, and a handful of years with > 2% and even 3%. But healthcare costs, childcare costs, even housing costs, have risen faster. And the delta between my 15% pay raise and my 400% deductible increase, or 200% childcare cost increase is where there emerges a crisis. If I interact with the healthcare system in an odd way, so as to avoid paying a deductible, or I let my personal debt accumulate, or I fail to finish my or online Bachelor’s, because of the demands of my family and job, I may be falling into a systemic vicious cycle that sets me behind, exacerbated by wealth inequality, but driven by the fact that my job simply doesn’t pay enough to help me get ahead. In this way, the national job statistics may tell an optimistic story about the economy, but there remains a gap for large swaths of the population.

Why have wages stagnated? Are the pressures of globalization really a factor? Does the fact that it’s cheaper to make clothing in Vietnam, electronics in China, customer service in India, et cetera, really push global wages down that far? Are the pressures of technology the driving factor? If technology has begun to automate away formerly high-paying or wage-accelerating jobs, which ones are they? Is that the missing Rust Belt story? These questions are endlessly complex, and I hope I can unpack them live (with you!) while I try to understand the state of today’s political economy; the dying dregs of Economy 2.0 are showing many signs, but I don’t feel clear on what is actually happening, or what that means for Economy 3.0. A month ago I thought the US econmy was recovering,a nd goign to be fine. today, I feel very pessimistic. Donald Trump’s election is a function of that, of course, but only in that it cataylzed me to start thinking about this. I happen to believe (and the data confirms) that Donald Trump won because of racism and cultural issues, not the economy, but I do still think we have a big question hanging over us. And I have to believe the answers are among the most pressing of our time. None of the coherent neoliberal economic narratives today balance sufficient compassion for the struggling worker with the amazing wealth accumulation, value-creation, and innovation the economic centers of the world are in the midst of. And if the optimists about technology, globalization, and social equity want to have it all, we need to have this story sharp, and it’s still very fuzzy today.

If there’s anything in the above that I’m misunderstanding, please feel free to jump into the comments or write me directly. I’m learning out loud, here.

This past week, I met with a few executives from a portfolio company to discuss the implications of a Trump Administration on the company. The conversation really struck me, particularly a few pieces:

At a personal level, they felt compelled to protest and organize, to take a stand against hate and separation. They felt guilty that it seemed like a mutually exclusive choice between being effective business leaders while also showing moral courage through their personal expression. They worried that creating a space for political dialogue might distract employees from work, but also that discouraging that space was even worse. They worried that creating a *safe* space for political dialogue might exclude those who voted against the rest of their peers at work, in whichever direction. It got me thinking: as a leader in a business, what responsibilities, or opportunities, do you have to your employees and peers in light of this election season? Is it okay, or even necessary, to take a stand?

What I suggested to them: remind your employees that gender discrimination has no place in the office, and will not be tolerated. Reassure them that you will fight for their work status, if they are immigrants. Commit resources to it, if you haven’t. Assure them that anti-discrimination in hiring and in human resources are the hallmarks of an empowering culture, and *will* drive better business results, particularly at a time where huge swaths of the community are uncertain about the future. Let them cry at work. Tell them that, no matter what their views, it’s natural to be afraid, to be angry, to feel betrayed. Give them space.

Executives have an opportunity to be bold in the workplace, with all of the power of the law behind them, and to double down on their investments in their people’s safety, freedom from persecution for their identities, and their economic security. These tactics can transcend politics, because they are a matter of universal human decency, but also of great business fundamentals. Mayors of many of the greatest cities in the United States, themselves CEO’s of municipalities, have taken similar proactive stances, to serve and protect their residents. Marty Walsh has put social justice and equality at the center of Boston’s agenda. Mayor Walsh is a former union worker, a white working class Dorchester man who lives in the neighborhood where he grew up, and knows a thing or two about what drives today’s American worker. I tip my hat to you, Marty. That is leadership.

As we transitioned the conversation to personal matters, they described the guilt they felt, to the guilt that I feel, too: that I’m not doing nearly enough. That I let every one of my black and brown brothers and sisters down when I have an inclination to lower my head, to accept the status quo, to put peace ahead of justice. That I let my wife, my mother, my sisters and my sisters-in-struggle down in every word I don’t say about the misogyny catastrophe that has gripped the nation, and maybe the world, for so many generations. I said to them, and really to myself: it’s okay to fight like hell. It’s even necessary. Take a personal day and go to a march. Take a personal day and go visit a prison through Defy Ventures. And bring a friend. Give your money to the ACLU and the Equal Justice Initiative. Listen to Bryan Stevenson. Take your daughters and sons to the million woman march on Washington. Keep the phone lines of your congressmen and senators so jammed they can barely do anything else but hear your voices. Because otherwise ***they want bury you***. And don’t lose hope, either. Because the famous quotation stands now more than ever: “they tried to bury us, but they did not know we were seeds.”

When it was Arab Spring, when it was the Green Revolution, even when it was Brexit, we laughed from our perch of moral superiority, back-clapped over how the genius of Facebook and Twitter sowed the seeds of direct democracy across the world. But what of now? What have we done? Does it occur to you that the cosseted and cloistered elites in the palaces of the Middle East and Great Britain, in the technocratic glass offices of Brussels might in fact be *you*? Has it occurred to you that democracy is, like any force of devastating power in our society, not always the good you had hoped it would be? The tyranny of the majority can be tyrannical, after all. The reality is, indeed, that power is, in the way we understood in the 20th Century, over. Even in the United States. The rules of political engagement for the Information Age are still being written, but most certainly don’t look the way the rules of engagement looked for previous political generations. They said Occupy Wall Street had failed. But Bernie Sanders actually came close to becoming our president, despite a massive traditional infrastructure ensuring he wouldn’t. Donald Trump spent very little money, and some might argue he simply tweeted his way to the Presidency. The rules are different this time.

One thing is for certain, though. We have the numbers. The Millennial Generation, the world over, is the biggest in the history of the world. We value and crave connection before all. We intermarry across racial and religious lines, we pray to many Gods. Our women are grabbing the mantle of leadership across sectors. We know how to organize at massive scale effortlessly – after all, we live and breathe memetic theory. And we may have just woken up.

For those of you who feel low, unable to sleep for fear for your families and loved ones, for those who are sick to your stomachs, so angry that you’re paralyzed: good morning, you are now what they call woke. Stay woke. The First Amendment of the United States constitution is the first for a reason. It is the cornerstone of a free and just society. The protection is not just of the right to speak, but to pray, to publish, and to protest. I fully intend to do all of those, and invite you to join me. Especially in these times.

***Don’t get it confused that President-Elect Trump didn’t mean what he said; at your peril do you take comfort in the belief that the “traditional Republicans” will “normalize” Donald Trump. It was a campaign of separation, hate, division, and phobia. And Bannon and Sessions are fully stark evidence that it will be an administration of the same. They want to bury us. Period.***

As recently as last year, smartphone sales globally grew 14%, and while that growth has slowed this year, it is a growth rate on over a billion devices, meaning over 100 million new devices hitting the market per year. That is an extraordinary shift, invites a new paradigm for connecting our world that we are still just beginning to understand.

If putting a personal computer in every home enabled the creation of the Internet economy (Amazon, Google, Facebook), putting a personal computer in every pocket in the world is enabling the creation of a new economy as well. At the infrastructure level, we have seen the self-driving car race serve to develop a data transmission control protocol like TCP/IP. Indeed, microsatellites, fiber optic and ethernet cables, CCTV networks, and mapping services like Waze and OKHi, will continue to add robustness to the core infrastructure layer, as well. The application layer enabled by this infrastructure is hard to imagine today, but will soon proliferate as fast as ecommerce, search, and social did before. And there is still more coming.

Today, we still use a version of a cell tower framework developed in the 1940s and 1950s by Bell Labs (now part of Nokia, founded by Alexander Graham Bell) for connectivity. Most of the national carriers have base station infrastructure that they have signed long-term contracts for, or bought outright, and have amortized the cost of this extremely expensive hardware over 25 years of monthly bill payments. But we all have *supercomputers* in our pockets, and there is sufficient density of those computers that we can do interesting things not only at the application and transmission control layer, but at the infrastructure layer, too!

When Daniela Perdomo pitched us GoTenna, she spoke about a world where a piece of hardware that could fit into your hand, featuring two very simple pieces of hardware – a mesh radio and a BLE beacon – could be sold to create a communication network that was fully bottom-up, with no need for third party mediators or someone to “offer the service”. Of course, this is relevant for disaster resilience, but also for rural neighborhoods where base station cell tower infrastructure does not have the density to justify extending the service (see my partner and our friend Kunal on the topic: https://www.fastcoexist.com/3063688/why-clintons-promise-to-provide-high-speed-internet-to-all-americans-is-so-necessary). And finally, in cities like New York, where we are always looking for ways to make density and connection useful to all parties, we can create mesh networks for schoolkids, church parishioners, and co-op neighbors to communicate for free, in private, and on their own.

At Collaborative we are obsessed with technology enabling a better culture for consumers of all types. Connecting to the Internet is getting closer and closer to a basic human right with each iteration, and we love supporting infrastructure that makes it accessible to all. And the nerdy side of us believes that IoT is not only coming, but that we have been thinking too small, and it could be as big as the Internet, indeed. GoTenna satisfies both the geek and the humanist, so I’m supporting their Kickstarter, and hoping you do, too!

I was having a discussion with my wife this week about this topic – she is in medical training right now, so when she comes from the hospital the topics are always interesting.

If you consider someone as a patient, there is a sacred, Hippocratic, oath that defines the relationship. The white coat represents more than a simple transaction, but a level of trust, honor, and responsibility that we have built into our society. As an outcome of that, however, sometimes a doctor takes a paternalistic view on their relationship with patients: they know what’s best, and that’s that. On some level, I’m sure you have witnessed this. And for the most part, it’s good, right? But that’s not how a market-driven relationship works. In a customer-based relationship, the work is in service of the customer, who is always right– so, the exact opposite. It is their money, after all.

We were discussing how it would be *so nice* if care providers, and the healthcare system more broadly, treated patients as customers. Among the seemingly endless issues with modern healthcare, many point to the fact that the patient is not a customer, as they are in other industries. And thus, creating a system that optimizes their needs is much lower priority, since they are simply a passive participant in a machine where they lack agency. So what if they had agency? Perhaps the level of service, the resources, and the general efficiency of the system would improve for those who had the ability to pay. But is that true? First of all, would that improve the system for everybody? Not only that (which is a political economy question), but secondly, do we even want that? A chef or driver insisting that I advise them on the best way to prepare a meal or travel to a destination is great, but a doctor asking me whether I should get a procedure? Surely not, right?

As an analog, we considered the schoolteacher. In a student-teacher relationship, a student relinquishes an element of agency: they do what they are assigned, with the implicit understanding that it is for their benefit, whether or not they can obviously see that. The most celebrated educators in the world still hold this cache, and teach whatever they want – and sometimes that is driven from a rational economic marketplace, but oftentimes it isn’t. Plenty of tenured (or similar) professors at our most prestigious institutions are shit teachers, if you stack them against a field of peers. And some students feel the weight of honor and sacred power in doing what the teacher says, and will spend 25, 30 years doing that. But others less so.** A college sophomore might think they only need computer science courses for their education, and as a consumer in an open marketplace, surely they ought to be able to choose, and society will be the better for it, right? What of an 11th grader? Or a 9th grader? Or a kindergartener’s parents? If you think this is a false equivalency, and ‘student’ should in fact be a ‘consumer’ but ‘patient’ should stay sacred, what is different? If you think the opposite, why?

I don’t know my answer to either yet: I lean towards customer/consumer for both scenarios, and believe that if you give me more agency and resources to understand my body, I ultimately know it better than anybody else, and thus ought to be able to decide about all of it. Similarly, there are infinite learning styles and ways to become an educated and productive member of society, and more choice ought to be better than less. But I’m not sure. The honor (really), trust, and sacred nature of the oaths care providers and educators take in caring for our society have real power, and I hope they aren’t lost in the shuffle.